irony.com has a clever cartoon touting the benefits of index funds:

While talking heads like Andrew Feinberg of Kiplinger's brag about how he and his brother "beat the dickens out of the market" and a financial advisor tells me how "easy" it is to beat the S&P 500, I still say that low cost index funds are the best choice for most individual investors.

I'm sure that most of us have been targeted by the Capital One prescreened credit card offer junk mail machine. Over the weekend I found out an interesting factoid from an acquaintance who is a Capital One employee: their internal estimates show that Capital One unsolicited mailings represent 1% of the total United States domestic mail volume!

Wow! While Capital One is infamous for its high volume of junk mail containing preapproved credit card offers with varying packaging, interest rates, fees, and terms, I had no idea that their junk mail carpet bombing strategy generated such a large percentage of domestic mail.

By the way, did I mention that I've had a paperless car loan from Capital One Auto Finance for a few years now?

When I bought my car, I agreed to a lower interest rate in exchange for agreeing to a statement-free loan with monthly electronic payments. The interest rate and customer service that I have received from Capital One Auto Finance has been excellent, but it is ironic that a company known for its high USPS mail volume offered me a better deal to keep our relationship electronic.

Now, what about those of us that aren't a master of the 0% balance transfer and want to stop the junk mail madness? The 2003 Fair and Accurate Credit Transaction Act has you covered. It offers an easy way to electronically opt out of these prescreened offers for a five year period. Check out OptOutPrescreen.com for the scoop.

When I started blogging a couple of months ago, I envisioned myself cranking out one useful post after another: sharing deals and strategies, discussing relevant financial news, sharing financial moves I am considering, etc.

Well, the honeymoon is officially over. Some days it feels like I'm in a blogging rut, where it is difficult to come up ideas that will translate to useful content. This is hard work!

How do you actually come up with something worth saying without resorting to useless "Amazon.com Friday Sale" posts? For now, I guess I'll dive into the archives of a few established blogs to find some inspiration.

Is the job market as strong as the President claims?

With the November elections coming up, President Bush seems to be on TV quite a bit lately touting the strength of the economy. While he indicates a strong job market due to the shrinking unemployment rate, naysayers claim that he is ignoring falling job creation numbers.

As an IT consultant, I have been seeing a pretty good supply of contract jobs available lately, although pay rates are still below their year 2000 levels. While I am making less money than I did six years ago, my skills and experience have continued to make me very marketable.

At the other extreme, I have a former colleague who has joined the invisible unemployed as he was laid off early in 2006 and is still struggling to find work. Since his skills and references are quite good, I have to wonder if a slowing job market or age discrimination is contributing to his job search woes.

So, what is it like finding work in the job market today?

All other MBNA cards can now be accessed at ibsnetaccess.com, which is a rebadged version of the old mbna.com web site.

I think this is great news, and I will continue to take advantage of the float that Bill Pay Choice provides as long as Bank of America continues to offer it.

Free Malt-O-Meal breakfast cereal can be had at Shaw's Supermarket until October 26th.

Although most people have probably never bought Malt-O-Meal cereals before, they should taste familiar since Malt-O-Meal has a product line with their own versions of many well known name brand products. For example, Malt-O-Meal Honey Nut Toasty O's says right on the package "TRY ME If You Like Honey Nut Cheerios cereal".

This great deal is possible because of a periodic Malt-O-Meal sale at Shaw's combined with Malt-O-Meal coupons from the SmartSource Sunday newspaper coupon inserts.

Shaw's has selected varieties of Malt-O-Meal cereal (12 - 18 oz. bags) on sale for $1 each this week. The sale price combined with Save 50¢ on ANY Malt-O-Meal Cereal double coupons from the 7/30, 8/20, or 9/17 SmartSource coupon booklets will make this cereal free.

Even if you are not a cereal lover, this freebie will make a nice donation to a local food pantry. Time to stock up!

We use home heating oil to heat our house and hot water. Our oil tank is topped off three or four times per year, to the tune about about five hundred gallons annually. That may not sound very expensive until you consider how much heating oil prices have skyrocketed over the past few years.

I initially paid about 50¢ per gallon for heating oil, which rose to $1.19 per gallon three years ago, and peaked at about $2.50 per gallon last spring. The result is that it now costs more for a single oil delivery than it did for a one year supply of heating oil in 1999!

I have been getting my heating oil from the same company since I bought the place, and several local price searches via telephone have shown that they have very competitive prices for oil delivery and 24 hour emergency service without requiring a contract or a budget plan.

I have also been comparing regional oil prices at NewEnglandOil.com and see that the prices there vary from 11¢ less to as much as 38¢ more per gallon than the latest price quoted to me by my oil company ($2.04). Knowing that, I am comfortable sticking with the same company since it is not worth the $55 dollars per year that I would save by switching to the company with the lowest price.

Driving a clunker is frugal, but emotionally draining

I bet we all know friends and neighbors that seem to be driving a new car every three years. While I would love to join them in their new car bliss, I try to keep driving my cars until they become unsafe or unreliable. My reason for doing this is simple: it is almost always cheaper to fix your existing car than to buy a new one (see Keep your old clunker or buy a new car?).

I drive an eight year old Nissan that I like a lot. It is reliable, fun to drive, and best of all it is 100% paid for. Until recently, this car has only required basic maintenance to keep it in top working condition. Unfortunately, that changed in July when my Check Engine light came on. Luckily, I was able to buy the parts and repair it myself, which was a frugal (and rewarding) way to address the problem.

All was well until my Check Engine light came on when I was driving home on Monday night. Based on the error code I pulled from the Engine Control Unit (ECU), I bought a new oxygen sensor for $70 and spent an hour installing it on Tuesday (hence no blog post) with the hope that it will fix my problem. I am happy to report that I am once again free of error codes!

The tough part is that my Nissan needs to pass a state emissions inspection next month. I admit that I'm worried another error code will pop up before then and I will be looking at an expensive repair bill to get it to pass inspection. Logically I know that it makes financial sense to keep repairing my old car, but I do miss the days when my Nissan was 100% worry free. That won't stop me from keeping my fingers crossed until I pass that damn inspection though.

September CPI-U numbers released: Pass on October 2006 I Bonds

The U.S. Bureau of Labor Statistics released the September 2006 Consumer Price Index (CPI-U) inflation data this morning, which decreased by 0.5% last month.

As I have mentioned before, now is one of the best times to consider purchasing I Bonds. The reason for this is that we now know what the rate of return for October 2006 I Bonds will be for both the first and second six month periods, which is important since I Bonds must be held for 12 months before they can be redeemed.

Using the CPI-U data from March 2006 (199.8) and September 2006 (202.9) (courtesy of inflationdata.com), we can calculate the variable rate for the second 6 month period for October 2006 issue I Bonds:

That would mean these bonds would earn a rate of 2.41% (1.40% fixed + 1.01 variable) for the first 6 months and 4.50% (1.40% fixed + 3.10% variable) for the second 6 months. This is obviously not an attractive rate considering that several online savings accounts are currently earning 5%.

Based on that, I don't think it makes sense to purchase October 2006 I Bonds. It is worth re-evaluating I Bonds in late November 2006 though, since it is possible that the Treasury will set an attractive fixed rate for November 2006 issue I Bonds. However, if the Treasury lowers the I Bond fixed interest rate portion (like I think they will), it may make sense to wait until late April 2007 before buying more I Bonds.

MBNA Bill Pay Choice: About to disappear next week?

I have been using the bill pay feature of my MBNA credit cards to pay some of my bills for about three years now, which has allowed me to use my credit card to pay my electric bill, other credit cards, and even my monthly mortgage payment! I may not earn any credit card rewards with this strategy, but it has enabled me to have an extra month of interest-free float for some of my cash.

Unfortunately, I believe that Bank of America will kill this great deal on October 23rd, when they transition all MBNA credit cards over to the Bank of America web site. Although I am not 100% certain that Bank of America will kill this program, I think it is very likely that I will soon lose the ability to put a November mortgage payment on an MBNA credit card and not have to actually pay for it until December.

Since I doubt that Bank of America will continue to provide consumers with such a great deal, I will be setting up a couple of MBNA Bill Pay Choice transactions this week in case this functionality disappears next week, and I encourage anyone else who uses this strategy to do the same.

Yesterday I came clean about the worst stock pick I have ever made. Today, I'd like to try and redeem myself with the best stock pick I have ever made: Procter & Gamble (PG).

In early March 2000, the PG stock price dropped by about 30% in one day due to a disappointing earnings announcement. I immediately sensed a buying opportunity since this was a pretty dramatic plunge for a company with such widespread market share and brand recognition in the consumer staples area (Pampers diapers, Crest toothpaste, Tide detergent, Bounty paper towels, etc.).

Two days after the price collapse, I bought 60 (split adjusted) shares of PG. I then bought 60 more (split adjusted) shares of PG in late June 2000 when the share price dropped about another 7%. Today, when I look at the 10 year chart (courtesy of nasdaq.com), I can see that I bought PG at its two lowest price points since January 1997!

I still hold PG to this day, and I am up 134% (including dividend reinvestment) since my original purchases over six years ago. In this case, I believe that two critical factors contributed to my stock picking success:

The market can be irrational: I bought the stock of a quality company at a steep discount after the market overreacted to a poor earnings announcement.

I bought stock in a best of breed company that I believed would rebound due to a strong product line and brand recognition.

The ironic part of this stock pick was that I made a good decision for the right reasons when I bought PG in the first half of 2000, but I seemed to forget this when I blundered and bought Lucent Technologies for the wrong reasons in the second half of 2000.

Although I had mainly invested in mutual funds up to that point, in 1999 I decided to embrace the stock market euphoria and opened an online brokerage account to purchase individual stocks. I felt empowered when some of my stock picks had done well, so I decided to purchase 40 shares of high-flying Lucent Technologies when its stock price dipped a bit in August 2000. One month later, I saw that this great stock had actually gone down a few more bucks per share, so I bought 60 more shares.

Of course, the chart (courtesy of nasdaq.com) shows what a horrible investment this turned out to be and I learned a valuable (and expensive) lesson at the hands of Lucent Technologies. I finally gave up on this dog last year, and ended up taking a loss of about $4,000.

Not long after my investment in Lucent, I came to the realization that I'm better off getting exposure to the stock market through low cost mutual funds. Although I did pick some stocks that have done very well (like ORCL, LOW, and PG), I haven't bought an individual stock in 6 years. I admit it: I'm just not very good at picking stocks.

Here are my current financial assets as of the market close on October 10th, 2006:

Asset

Sep

2006

Oct

2006

Change

Checking

266

451

185

Money Market

44,052

19,016

-25,036

Savings Bonds

16,845

15,795

-1,050

Treasury Bills

26,000

21,000

-5,000

CDs

10,000

40,091

30,091

Brokerage

84,061

88,014

3,953

401k

86,143

89,010

2,867

Roth IRA

25,118

25,747

629

SEP IRA

127,829

135,995

8,166

529 Savings

27,672

29,026

1,354

Total Assets

$447,986

$464,145

+$16,159

(3.6%)

The strong stock market once again gave my investments a nice boost over the past month and I have continued rotating my cash holdings out of I Bonds and T-Bills and into a high yield CD ladder.

I also sent in a contribution to my SEP IRA yesterday, so I should should see a bit of a bump there next month.

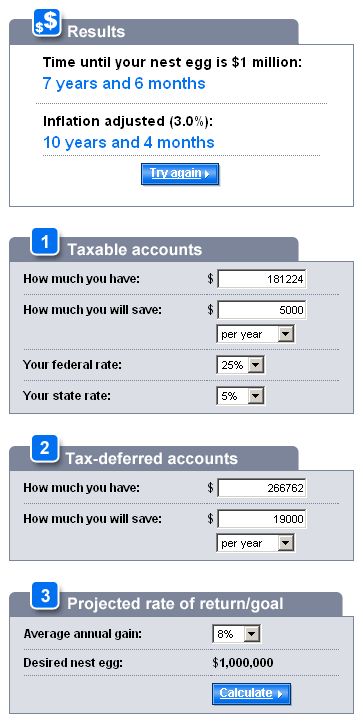

As I mentioned yesterday, I have a chance to become a millionaire in April 2014. That made me wonder what my financial position was like when I look back over the same time period, taking me back to April 1999.

In April 1999, I had assets totaling $104,898 ($43,418 taxable $61,480.69 tax-deferred). With my September 2006 asset total of $447,986, that gives me an asset growth rate of 327% over the last seven and a half years! Although I haven't broken out new contributions vs gains during that period, I believe that the majority of this growth has come from investing new money in mutual funds during the stock market slump in 2002-2003.

While I haven't crunched all of the numbers, my theory is based on the behavior of a 401k account of mine from a former employer (which I haven't contributed to since 1999). While my overall asset total has grown by 327% since April 1999, this 401k account has only grown by 42% over this same time period (including 31% over the past two years).

Even though my asset total has grown to a pretty nice level so far, I am convinced that continuing to add new money to my savings and investments is just as important as growth via compounding. I will be counting on growth in both areas (and a little luck wouldn't hurt) if I want to become a millionaire by 2014.

"The future belongs to those who believe in the beauty of their dreams." -- Eleanor Roosevelt

According to the CNNMoney.com Millionaire Calculator, I will join the millionaire club in April 2014. Obviously, this is a very basic tool that makes quite a few assumptions, but it is an interesting data point to consider.

The calculator came to this conclusion assuming an annual 8% return using the account balance data from my September 2006 Financial Asset Roundup, my 2005 income tax brackets (5% state, 25% fed), and estimated annual savings contributions ($15k SEP, $4k Roth, $5k taxable):

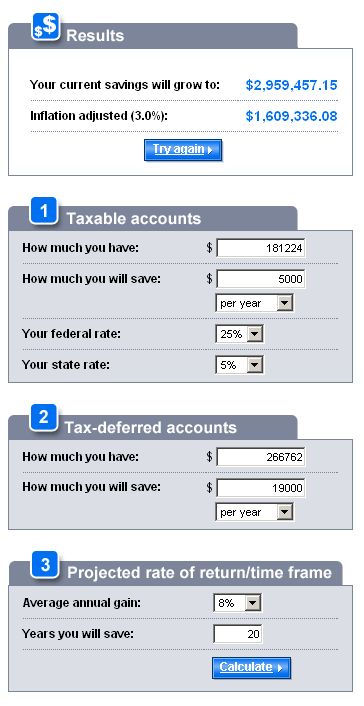

I also wondered where I would be in twenty years. Using the same data with the CNNMoney.com Savings Calculator, I will have almost 3 million dollars in the year 2026:

I realize that many things can change in the next twenty years, but it is pretty good motivation to see the rewards of saving and investing over the long term. The best part is that these numbers could be on the conservative side if and when my wife returns to the workforce.

The Diehards Forum is a community full of helpful people that want to see you succeed in your financial journey. If you post a question, you can be sure to get many opinions and recommendations on bonds, mutual funds, asset allocation, retirement planning, investment risk, and just about any other topic you can think of.

However, there is one thing I don't like about the Diehards forum: the blind pro-Vanguard bias that some Diehards (understandably) have. I always strive to get the best deal for my money whether I am buying a car, a mutual fund, or a tube of toothpaste, and it can be frustrating when I see someone who doesn't let the facts get in the way of defending their pro-Vanguard position.

For example, Fidelity lowered expense ratios to 0.10% for its Spartan index funds two years ago, which were lower than some Vanguard index fund expense ratios. Although Diehards should be pleased that Vanguard's low cost index funds were the main reason that Fidelity made this change, there are some that dismiss the facts and imply that Fidelity is doing this to mislead potential investors (see: Fidelity index funds lower cost than Vanguard). The fact is, Fidelity's lower expenses bring more competition to the market, which is good for everyone. And no matter what some Diehards say, a good deal is a good deal (even if it's not from Vanguard).

Showtime is offering a Free Preview Weekend starting tomorrow, October 6th and ending on Monday, October 9th.

If you are a DirecTV customer like me, all programming on channels 537 - 549 (Showtime, The Movie Channel, FLIX, and The Sundance Channel) will be free for the entire weekend, so fire up your TiVo and get the most out of this promotion. Enjoy!

Why not join the free Upromise college savings program and take the bonus buck that they're offering? It's not much, but Upromise is a nice way to earn a little extra money when doing things like buying groceries, dining out, and shopping online.

Although Upromise touts itself as a 529 college savings program, they do not require participants to open a 529 college savings account. The entire balance of your Upromise account can be withdrawn at any time by requesting a check, which you can then invest as you see fit.

Here's how it works:

Clink on one of the links below to open a Upromise college savings account and to qualify for the $1 bonus credit:

If all of the above links return an error, then please post a comment before signing up for a Upromise account so you can get your free $1 bonus. I will post additional referral links as needed.

The reason is pretty clear when you look at Ing Direct Orange Savings Account Yields for the past four years:

Although 5% yields have made cash a nice place to be in 2006, the above data shows this hasn't been the case since the FOMC started cutting the Federal Funds Rate in 2001.

We are now seeing hints of another FOMC rate cutting cycle, which has caused Treasury and CD rates to drop since August. Seeing that, I tried to learn from past experience and decided to lock in existing rates for some of my cash holdings by building a 4 year CD ladder.

Over the last few weeks, I have bought 1,3, and 4 year CDs with a 6% yield in equal dollar amounts. Today, I completed my 4 year ladder by opening an E-LOAN 5.75% APY 2 year CD.

The result is a 4 year CD ladder with equal amounts invested as follows:

Knowing what I know now, I wish that I had the foresight in late 2000 to lock up some cash in CDs yielding 6% when the economy was showing signs of slowing down. If savings account yields fall below 2% again (like Ing did in August 2003), I will feel like I made a wise decision. And if yields happen to rise, then I can always reinvest my 6% CDs at the higher rates when they mature over the next few years.

New England AAA members: get a car checkup for one dollar

October is AAA Car Care Month, and AAA Southern New England members can get their car inspected at an Approved Auto Repair facility for one dollar. A quick google search shows that AAA branches all over the country are offering cheap or free Car Care Month maintenance inspections that might be worth looking into.

I also received a separate mailing from a local car dealer (an AAA Approved facility) that is offering a no cost 100 Point Courtesy Check-Up during the month of October. I am assuming that this offer is similar to the $1 checkup that AAA is offering.

According to the dealer mailing:

Bring your Nissan to our dealership and, in one quick visit, your vehicle will receive a complimentary, 100 Point visual inspection.

Factory-trained technicians will thoroughly examine everything from tires to brakes, from exhaust to electrical, and present you with a written diagnostic repost at no cost or obligation to you. With a superior understanding of your vehicle, you can drive confidently knowing your Nissan is operating at its full potential.

Although I am no fan of car dealers, I may take my local Nissan dealer up on their free inspection offer. I know that I was relieved a few years ago when the dealer spotted a gash on the inner wall of my tire that was not visible until the tire was removed from the car. Even though they wouldn't make any money on its replacement, they recommended that I have it replaced by the tire shop where I bought it as soon as possible.

Bank of America/AAA high yield money market savings account

As of September 22nd, the MBNA/AAA Cash Maximizer® Savings account has been rolled into Bank of America. So far, it appears that this account will not be a casualty of the Bank of America purchase of MBNA.

According to the AAA sign up link, the Cash Maximizer® account is currently paying the following rates:

Daily Balance

Current Interest Rate

Annual Percentage Yield

Less than $2,500

4.48

4.57

$2,500 - $9,999

4.73

4.83

$10,000 - $49,999

4.98

5.10

$50,000 and over

5.23

5.36

This weekend I finally bit the bullet and signed up for the account. As a Bank of America customer, this account is particularly attractive to me since it offers a 5.10% APY for balances over $10,000 and allows instantaneous transfers to a linked Bank of America checking account via their online banking service.

I don't know how long will Bank of America keep this great deal in place, but I'm hoping that MBNA had a deal with AAA that will require Bank of America to continue to offer this account for the foreseeable future. I wouldn't be surprised to see it disappear though, since Bank of America offers rates much lower than online competitors like HSBC and EmigrantDirect for its other checking and savings accounts. I'll use it as long as I can, but I'll also be keeping my fingers crossed.

I cashed in the I Bonds that I bought in July 2003 today. Based on the criteria I discussed in an earlier blog entry (Should You Sell Those Savings Bonds?), today was the day to sell my July issue bonds.

Since I haven't held them for the required minimum of five years, I had to forfeit the last three months worth of interest. I cashed them in today because I end up sacrificing three months worth of interest at 2.11%, while keeping all interest earned at the previous rate of 6.83%.

Since I have started moving some cash to 6% CDs while they are still available, I will be cashing in all of my I Bonds over the next few months due to the low rates that they are currently earning. My August 2003 I bonds are next in line and will be cashed in on November 1st.